On November 7, 2022, the Financial Services Agency (FSA) published a draft amendment to the Cabinet Office Ordinance on Disclosure of Corporate Information, etc. The draft amendment makes it mandatory to include "disclosure of corporate initiatives related to sustainability" and "disclosure related to corporate governance" in securities reports. The revised provisions will apply to securities reports, etc., for fiscal years ending on or after March 31, 2023. Further revisions will be made in the future, taking into account domestic and international trends.

This article summarizes and introduces the "disclosure of corporate initiatives regarding sustainability" in securities reports.

source:Financial Services Agency Announces Proposed Amendments to the Cabinet Office Ordinance on Disclosure of Corporate Information, etc.

The archived video of the seminar, which explains the content of the new sustainability information disclosure standards and what companies should do now to ensure appropriate information disclosure, is available here.)

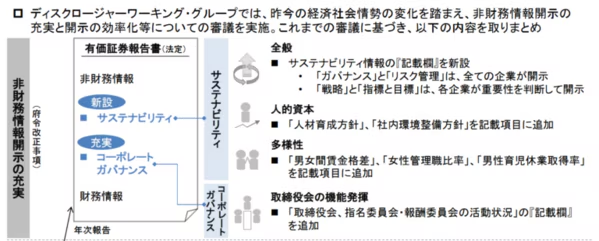

Disclosure of overall sustainability information in securities reports

First, a new "section for disclosure" has been created in securities reports as a framework for providing sustainability information in an integrated manner, and companies are now required to describe their approach to sustainability and their initiatives.

The framework is based on the same four components as the TCFD recommendations and the ISSB's exposure draft: "governance," "strategy," "risk management," and "metrics and targets."

The information to be disclosed is as follows:

- Required information: "Governance" and "Risk Management"

- Items to include according to importance: "Strategy" and "Metrics and Targets"

Regarding the new "section for sustainability information" in the securities report, if sustainability information is included in other sections, it is now permitted to refer to those other sections within the "section for sustainability information."

Furthermore, regarding forward-looking statements, which were previously difficult to include, it is now stipulated that "if such statements are included along with the facts and assumptions considered, it must be made clear that even if the actual results differ from the forward-looking statements, the company will not be immediately liable for false statements."

Disclosures regarding human capital and diversity in securities reports

Next, in the "Strategy" and "Metrics and Targets" sections of the "Description" field, the following mandatory information regarding human capital and diversity is required.

- Policies for human resource development, including ensuring diversity in the workforce, and policies for improving the internal work environment.

- Content of indicators related to the said policy

Furthermore, companies and their consolidated subsidiaries that publish the following indicators in accordance with the Act on Promotion of Women's Participation and Advancement in the Workplace, etc., are required to include these indicators in their securities reports, etc.

- Ratio of female managers

- Rate of men taking paternity leave

- Gender wage gap

Furthermore, you may optionally include additional information when describing the above indicators.

source:Financial Services Agency, "Summary of the 'Disclosure Working Group Report' - Towards the Construction of Capital Markets that Lead to the Improvement of Corporate Value in the Medium to Long Term" Created by processing

"Desirable disclosures" in securities reports

In addition to the required information, the revised proposal also outlines the "desirable disclosure efforts" regarding sustainability information disclosure as follows:

- Even if a company decides not to include "strategy" and "metrics and targets" based on its own assessment of their importance, it is expected to disclose the reasoning behind that decision.

- When climate change response is important, information should be disclosed within the frameworks of "governance," "strategy," "risk management," and "metrics and targets."

- Regarding GHG emissions, while taking into account each company's business type and operating environment, proactive disclosure of Scope 1 and Scope 2 GHG emissions is expected.

- Regarding diversity indicators such as the "percentage of female managers," in addition to disclosing company-specific indicators within the consolidated group, efforts should be made to disclose them on a consolidated basis.

(Addendum) The Financial Services Agency announced on January 31, 2023Publication of "2022 Best Practices for Disclosure of Descriptive Information" (Disclosure of Sustainability Information, etc.)We have published this information. It contains many good examples of sustainability disclosures in securities reports, so please refer to it.

Reference seminar:Current climate change disclosure responses

summary

Based on the Corporate Governance Code revised in June 2021 and the current proposed amendments, sustainability information disclosure is now positioned as one of the main items of corporate information disclosure in securities reports for all listed companies, not just those on the prime market.

Considering the effective date of the revised proposal and the need to establish sustainability systems, companies will likely need to take early action to expand their disclosure requirements.

At booost technologies Inc., we offer comprehensive sustainability consulting services to enhance corporate value, including support for ESG, TCFD, human capital improvement, and the creation of IFRS sustainability integrated reports and annual reports. We also provide a decarbonization support platform that enables automatic visualization of CO2 emissions and carbon offsetting.booost GXWe offer "[this service]".

If you have any concerns about disclosing sustainability information, please feel free to contact us.