Previous article "What is the EU's Carbon Border Adjustment Measure (CBAM)?In the previous article, we explained the overview of CBAM and its impact on Japanese companies. In this article, we will focus on the concept of "embodied emissions," which is particularly important within CBAM, and explain its definition, calculation method, and relationship with Scope 1, 2, and 3 emissions.

▼For a basic explanation of Carbon Border Adjustment Measures (CBAM), please read the article below.

What is the EU's Carbon Border Adjustment Measure (CBAM)?

You can download the solution documentation here.

● Service introduction materials for "booost GX"

Definition of embodied emissions

Businesses are required to report not only the quantity and type of CBAM-compliant products imported into the EU, but also the embodied emissions and the carbon price paid in the country of origin, in their CBAM reports. Therefore, it is necessary to have a proper understanding of embodied emissions.

Integrated emissions refer to GHG emissions generated in connection with the production of eligible products imported into the EU, and are divided into two types: "direct emissions" and "indirect emissions."

Direct emissions are those arising from the production process of the product in question. Regardless of the production location, GHG emissions resulting from the production of heat and cold during production are included in direct emissions. On the other hand, indirect emissions are defined as GHG emissions resulting from the generation of electricity consumed in the production process of the product in question. Regardless of the location of power generation, these must be included in indirect emissions.

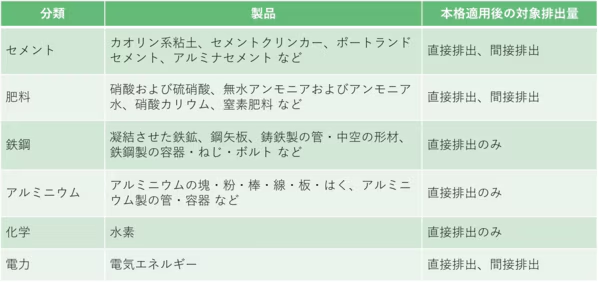

During the CBAM transition period, both direct and indirect emissions must be calculated and reported. However, after full implementation, some sectors (steel, aluminum, hydrogen) will only be required to calculate and report direct emissions, while the cement, electricity, and fertilizer sectors will be required to calculate and report both direct and indirect emissions. The following diagram summarizes the target emissions by sector, and we recommend that you review it again.

*Please note that you will need to check the CN code (EU tariff classification) listed in Annex I of the CBAM Regulations (List of goods and greenhouse gases) for details on the products covered.

Source: European UnionREGULATION (EU) 2023/956 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 10 May 2023 establishing a carbon border adjustment mechanism

Method for calculating embodied emissions

The method for calculating integrated emissions differs between products in the power sector and other sectors. For sectors other than power, there are two methods: calculation based on actual emissions and calculation using default values.

Calculation based on actual emissions

First, the following formula is used to calculate the amount of materialized emissions per ton of non-electric products:

After full implementation, the cement and fertilizer sectors will be required to calculate and report indirect emissions. However, actual indirect emissions can only be used in the following two cases. For all other data, default values must be applied.

- If you can prove a "direct technical link" between the production facility for the imported goods and the power plant.

- If you have a power purchase agreement with a power generation company located in a third country

The following formula is used to calculate the amount of material emissions from input materials. Only input materials listed in Annex II of the Implementing Regulations (Definitions and production routes for goods) are included.

Calculation using default values

For products other than electricity, if the actual direct emissions cannot be calculated, it is permitted to use one of the following default values for calculation.

- A value added to the cost based on the average emission units set for each exporting country for each product.

- The value is based on the average emission units of the worst-performing EU-ETS facility that produces the product in question.

- If it is possible to determine the optimal default value by using data that is tailored to the specific regional characteristics of countries outside the region, then use a value based on that.

The default value used to calculate indirect emissions is a value calculated based on the average of one of the following:

- EU power grid emission factors

- Emission factors of power grids in power-producing countries

- CO2 emission factors of price-setting sources in electricity-producing countries

Source: Japan External Trade Organization (JETRO) Explanation of the EU Carbon Border Adjustment Mechanism (CBAM) (Basic Version)

european union COMMISSION IMPLEMENTING REGULATION (EU) 2023/1773 of 17 August 2023 laying down the rules for the application of Regulation (EU) 2023/956 of the European Parliament and of the Council as regards reporting obligations for the purposes of the carbon border adjustment mechanism during the transitional period

Organization of integrated emissions and Scope 1, 2, and 3 emissions

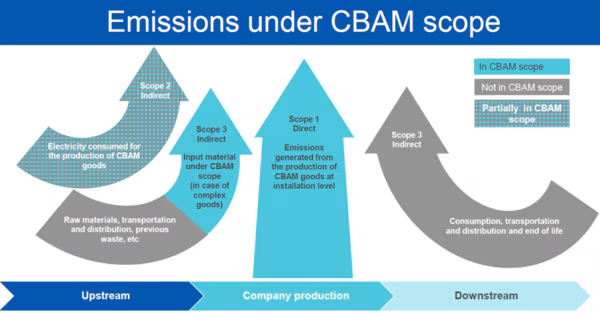

We have now discussed how to calculate direct and indirect emissions, which are necessary for determining embodied emissions. Some of you may be reminded of the concepts of Scope 1, 2, and 3 emissions under the GHG Protocol.

Here, we will explain the differences and connections between the two.

Scope 1 refers to GHG emissions from sources that an organization directly controls. Scope 2 refers to GHG emissions from indirect energy sources that an organization purchases or uses, such as electricity, heat, steam, and cooling.

However, CBAM direct emissions include all production of heating and cooling energy consumed during the production process, regardless of the production location. For example, if steam produced outside of a company's premises is supplied to a factory, it would be classified as Scope 2 under the GHG protocol, but under CBAM it is considered a direct emission.

Scope 3 covers all other indirect emissions that occur in a company's value chain, but only emissions related to electricity and heating/cooling consumed when producing input materials specified by the implementing rules are covered by CBAM.

Source: European Union Carbon Border Adjustment Mechanism A new, green way of pricing carbon in imports to the EU

summary

CBAM (Carbon-Based Amendment) imposes payments based on the carbon price difference derived from the incorporated emissions of targeted products. It is an important tool for promoting carbon emission reductions within the EU while simultaneously preventing carbon leakage. At present, the impact on Japanese companies is expected to be limited, but since the range of targeted products may expand in the future, companies exporting to the EU need to prepare early by working with their suppliers to collect data for GHG calculations.

booost technologies provides solutions that visualize CO2 emissions from facilities such as factories and offices in real time, broken down by time of day, equipment, and more. Primary data and actual measured values of CO2 emissions are securely acquired from sensors installed on each piece of equipment, via industrial routers and the equipment's API.

That data is used in our CO2 emission visualization and decarbonization platform,booost Sustainability Cloud It is possible to automatically import data and visualize CO2 emissions from primary data/actual measurements of factories and facilities. For more details on this initiative and a demonstration, please feel free to contact us using the information below.