The number of companies implementing third-party assurance for sustainability information is increasing year by year. An analysis of CDP's 2023 responses showed that more than 401 TP3T of Japanese companies had implemented third-party assurance for GHG emissions. Another survey of companies comprising the Nikkei 225 also reported that 66% had received some form of third-party assurance for sustainability information in 2023.

While third-party assurance is becoming less of a special case, there is also a trend towards expanding its scope and increasing its sophistication. Therefore, it is necessary to closely monitor future trends and the required responses. This article will explain the increasing demand for third-party assurance and what actions those responsible should take.

▼For a basic explanation of third-party guarantees, please read the article below.

What is third-party assurance in CO2 emission disclosure?

You can download the solution documentation here.

● Service introduction materials for "booost GX"

Regulatory trends surrounding third-party guarantees

This article will explain the trends in third-party assurance, focusing on systems that have a significant impact on Japanese companies.

Application of SSBJ standards

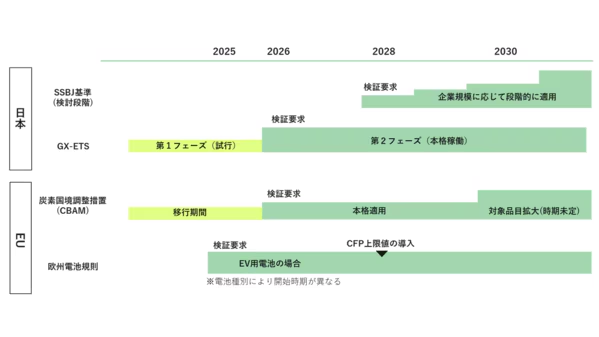

In 2023, IFRS S1 and S2, the new global standards for sustainability information disclosure, were published. Currently, the SSBJ is compiling the Japanese version of these standards, and the Financial Services Agency is simultaneously discussing their application. As a result, the disclosure of GHG information, including Scope 3, and other important sustainability information in securities reports and other documents will be gradually made mandatory depending on the size of the company.

Regarding third-party assurance, it is expected to become mandatory for large companies (market capitalization of 3 trillion yen or more as of July 2024) as early as 2028, and will expand to all prime listed companies by 203X. Since the boundary of this standard, like the disclosure of financial statements, applies to the entire consolidated group, improved accuracy in information gathering is required across a wide range of areas.For companies that have never obtained third-party assurance, including for their group companies, it will be difficult to obtain assurance for all consolidated organizations in the first year of mandatory implementation.It is possible that this could happen. It may be necessary to consider measures such as bringing forward the guarantee period by one to two years, having the guarantee institution conduct a trial guarantee, and identifying any issues.

Full-scale implementation of emissions trading scheme

The government has already decided in a cabinet meeting to fully launch a domestic emissions trading system in fiscal year 2026. Currently, the first phase (trial stage) is underway towards the full launch of the emissions trading market in fiscal year 2026, and the emissions trading system (GX-ETS) is being operated through the GX League, with voluntary participation from companies. Although participation is voluntary, as of March 2024, companies covering more than 50% of Japan's GHG emissions are participating in GX-ETS, making it a major system in Japan. In the second phase, which will begin in fiscal year 2026, some measures are planned to further increase participation rates, and these measures may include mandatory measures.

Under the emissions trading scheme, third-party verification will be required to confirm the achievement of GHG emission reduction targets and to generate credits. We expect that the number of companies providing GHG emission guarantees will broaden once the scheme is fully operational in fiscal year 2026.

Impact of European Institutions Related to CFP

In the area of GHG emissions, third-party assurances are expanding beyond organizational units to include products and services. As for carbon footprint (CFP) assurances, some are voluntary, while others, like those in Europe, are becoming mandatory.

Carbon Border Adjustment Measures (CBAM)Under European regulations known as CBAM, EU importers are required to report the GHG emissions of designated products imported from outside the EU. From 2026, when the regulations are fully implemented, third-party verification of the GHG emissions of products will also be required. Although the obligation to report to CBAM rests with the importers, manufacturers supplying the products will be required to provide accurate information regarding CFP.

Also,European Battery RegulationsTherefore, manufacturers and distributors are required to disclose the CFP (Chemical Function Plan) for various types of batteries. Third-party verification is also required for these CFPs.

Towards efficient third-party assurance assessment

As mentioned earlier, the increasing mandatory nature of third-party assurance is making it increasingly necessary. Obtaining third-party assurance places a heavy workload on company personnel, who must prepare various documents, act as liaison with auditing bodies, and communicate with the auditing locations. So, how can this process be made more efficient?

The necessity of establishing internal controls

When internal controls related to sustainability information—that is, governance systems, business processes, and IT infrastructure—are well-established, the risk assessment by the certification body will be deemed low, and the process will proceed efficiently. On the other hand, if internal controls are not in place and subjective data aggregation is evident throughout, the scope that the certification body must verify will expand, and the amount of work required for the assessment will increase.

To effectively and efficiently collect, disclose, and ensure sustainability information, it is crucial to have internal controls in place.

What is a third-party warranty support system?

Implementing appropriate systems significantly contributes to the development of internal controls and the rapid and accurate collection of information. So, what functions are required of a system that complies with third-party assurance requirements? Here are a few examples.

| function | explanation |

|---|---|

| Workflow-based approval | Authority settings and approval/rejection functions to ensure effective governance and internal control. |

| Flexible timeframe and boundary setting | To address the differences in aggregation periods and boundaries between domestic systems and global standards, a function has been added that allows for variable setting of periods and boundaries. |

| Supporting documents (invoice, delivery note, etc.) are attached. | A feature that allows you to manage data so that it can be immediately cross-referenced with the basis for data entry. |

| Input error prevention alert | A feature that allows you to set a threshold and display an alert when an abnormal value is entered. |

| Data Confirmation | A function to prevent data that has been reviewed and finalized from being overwritten or modified. |

To efficiently implement third-party assurance, various other functions are necessary in addition to those mentioned above. When considering the introduction or updating of a sustainability information aggregation system, it is important to check not only whether it can aggregate data, but also to what extent the design takes third-party assurance into consideration.

summary

There are several issues that companies must consider when institutionalizing third-party assurance. For example, since the rules (standards) regarding assurance differ depending on the system, separate assurance may be required for each system. Also, as assurance becomes more widespread, there may be a shortage of auditing bodies and auditors, making it difficult to undergo audits on the desired schedule, especially during peak seasons. Furthermore, some systems are looking beyond limited assurance to include a transition to reasonable assurance.

Implementing a system for efficiently conducting third-party assurance is one effective way to address these challenges.booost Sustainability Cloud(booost GX) not only includes the functions mentioned above, but also covers all the functions necessary for third-party assurance, and can greatly contribute to compliance with regulations.

For more details about our initiatives or to request a demonstration, please feel free to contact us using the information below.