The publication of the final standards (SSBJ standards) for mandatory sustainability information disclosure, scheduled for the end of March 2025, is fast approaching. Those responsible for Japanese companies aiming for sustainable management need to understand the schedule, plans, deadlines, target companies, and required responses for this mandatory sustainability information disclosure.

This article explains the overview of these standards and how companies should respond to them going forward.

Overview of SSBJ Standards

Since there are many articles explaining the background of the SSBJ standards' development and comparing them with international sustainability disclosure standards (IFRS S1, S2), this article will explain the outline and overall impression of the exposure draft using the 5W1H framework.

When: Application schedule and plans for SSBJ standards

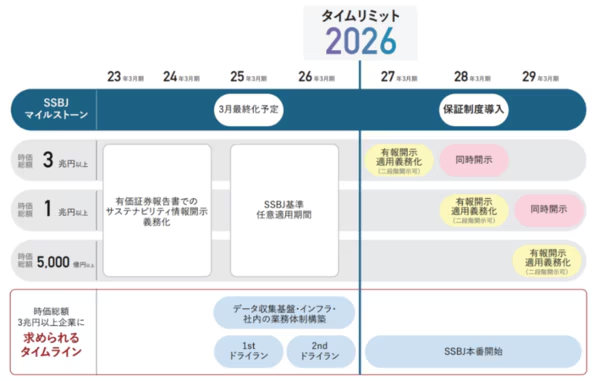

The SSBJ's final standards will be published by the end of March 2025, but they will not be immediately applicable. The mandatory implementation schedule is being considered by the Financial Services Agency's Financial System Council's Working Group on Sustainability Information Disclosure, and according to public documents [1], an application schedule based on the size of the company is being considered. The fastest companies (market capitalization of 3 trillion yen or more) will have a voluntary application period until 2026, and will be required to apply from the fiscal year ending March 2027.

Who (who) are the companies to which this applies?

The proposed SSBJ standards are being developed on the premise that prime listed companies or a portion of them will be subject to these standards, and will be expanded in stages, starting with companies with a market capitalization of 3 trillion yen or more, then 1 trillion yen or more, then 500 billion yen or more, and finally the remaining companies.

Specifically, the SSBJ standards will be applied to companies with a market capitalization of 3 trillion yen or more from the fiscal year ending March 2027, to companies with a market capitalization of 1 trillion yen or more from the fiscal year ending March 2028, and to companies with a market capitalization of 500 billion yen or more from the fiscal year ending March 2029.

<Schedule for responding to disclosures based on SSBJ standards>

Where: Location of information disclosure

Sustainability-related financial disclosures must be disclosed together with the relevant financial statements. While they don't necessarily have to be in the same document, the relevant financial statements must be identifiable. In other words, they must be included in the securities report.

What (Disclosure Items)

The SSBJ draft standards consist of three draft standards: the application standards, the general disclosure standards, and the climate-related disclosure standards. Here, we will briefly introduce the key points of each.

[Proposed application of sustainability disclosure standards]

In developing the application plan, references were made to the SASB Standards, CDSB Framework Application Guidance, GRI Standards, ESRS, etc., and disclosure of information was required not only related to climate change but also on sustainability in general. Furthermore, the following basic principles have been established regarding general disclosure.

- Reporting Scope: Applies when preparing and reporting sustainability-related financial disclosures in accordance with SSBJ standards.

- Reporting entity: The financial statements must be disclosed for the same reporting entity as the relevant financial statements, i.e., for the entire group.

- Timing of reporting:

Simultaneous reporting: As a general rule, financial statements must be reported simultaneously with the relevant financial statements.

Reporting period: As a general rule, the reporting period should be the same as that of the related financial statements.

[Draft for general disclosure standards]

The proposed general disclosure standards outline the fundamental requirements for sustainability-related disclosures. This requires companies to disclose sustainability information across four components: governance, strategy, risk management, and metrics and targets.

[Draft Climate-Related Disclosure Standards]

The proposed climate-related disclosure standards specify concrete requirements for strategies, indicators, and targets related to climate change. Of particular note is the pre-defined quantitative items for disclosing cross-industry indicators.

① Absolute total amount of greenhouse gas emissions

Disclosure of data categorized into Scope 1, 2, and 3, as well as disclosure of total values.

② Capital investment

Amount of capital expenditures, financing, or investments made in climate-related risks and opportunities.

③ Internal carbon price (if the internal carbon price is used in decision-making)

Internal carbon pricing and its application methods

④ Compensation (if climate-related evaluation criteria are included in executive compensation)

The percentage of executive compensation linked to climate change-related performance evaluation criteria and how they are incorporated.

The proposed General Disclosure Standards and Climate-related Disclosure Standards require that indicators be described as either absolute, relative, or qualitative. Furthermore, if third-party certification is provided, the name of the certifying body must be clearly stated; if no certification is provided, this fact must be indicated.

Why do companies need to disclose information?

As the importance of sustainability in corporate activities increases, with investors selecting investment targets based not only on financial information but also on non-financial information, such as ESG investing, there is a growing demand for prompt and accurate sustainability disclosure worldwide. Against this backdrop, the Sustainable Sustainability Board of Japan (SSBJ) was established in Japan to develop and publish disclosure standards. Moving forward, as related laws and regulations are being developed, efforts to make the SSBJ standards statutory disclosures are being considered by a working group of the Financial Services Agency's Financial System Council. If the SSBJ standards become the standard for statutory disclosure, companies will be compelled to disclose sustainability-related information.

How should companies respond?

In the previous section, we explained the overview of the SSBJ standards. In this section, we will explain how companies should respond. As mentioned in 1.4, the disclosures required by the SSBJ standards include a new dimension that differs from previous sustainability information disclosures. Therefore, the required response for companies is as follows:Accuracy(Improving the reliability of information)Speed(Prompt response), andsizeIt is necessary to emphasize these three points (comprehensive response to the target area).

Accuracy: The need for third-party assurance equivalent to that for financial information.

When disclosing information in securities reports under SSBJ standards, sustainability information is required to have the same level of third-party assurance as financial information. This necessitates the establishment of sophisticated internal controls, including appropriate approval workflows and data infrastructure, and penalty provisions are also being considered by the Financial Services Agency.

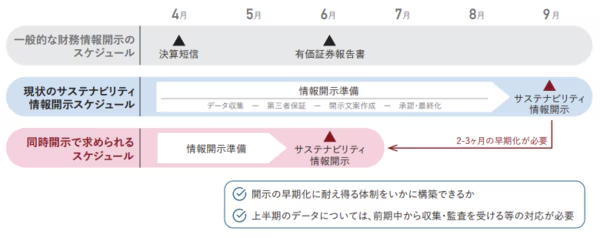

Speed: Simultaneous disclosure with financial information

Currently, many companies disclose sustainability information with a delay of about two to three months compared to financial information disclosure (submission of securities reports). The SSBJ standards require simultaneous disclosure of both financial and non-financial information, necessitating the establishment of systems capable of accommodating earlier information gathering.

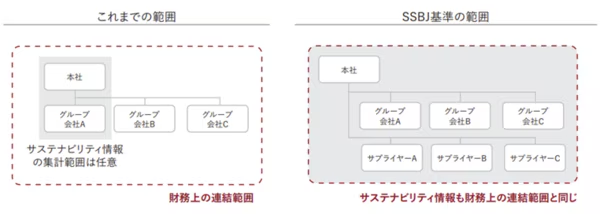

Scope: Disclosure within the same consolidated scope as the financial statements.

Compared to previous standards, the SSBJ standards significantly expand the scope of sustainability information collection. As shown in the diagram below, the items have expanded to include not only climate change but also sustainability in general, and the scope of aggregation is the same as that of consolidated financial statements, as well as requiring consideration of the value chain.

summary

In today's world, where the disclosure of sustainability information is required, basing a company on sustainability is key to its growth and competitiveness. We believe that establishing a "sustainability data platform" that enables accurate, rapid, and comprehensive data management, and driving projects through company-wide teams, are two crucial points that hold the key to achieving this.

Sustainability 2026 Issue

With the mandatory disclosure requirement coming into full effect in the fiscal year ending March 2027, companies should seize this as an opportunity to implement highly agile management reforms that leverage sustainability data. A crucial turning point for companies will be whether they can establish a data infrastructure, including suppliers, and a system for promoting Sustainability Transformation (SX) by 2026.

Sustainability 2026 Issue: "Making Japan a Leading Nation in SX" Project

Related Pages

Please also read the related pages for this explanation.

For those who want to know about measures to address the SSBJ regulations.

What are SSBJ standards? An explanation of the requirements for sustainability disclosure.

This is for those who want to learn about the concept of sustainability management through the use of data.

Data utilization and key points for achieving sustainable management

This is for those who want to know how to calculate greenhouse gas emissions (CO2 emissions, etc.).

How are CO2 emissions calculated?

This is for those who want to know about the process of third-party assurance for greenhouse gas emissions (CO2 emissions, etc.).