「How will mandatory sustainability disclosure affect Japanese companies?In the article, we explained the overview of the SSBJ standards and their impact on Japanese companies.

This article explains the necessary measures for companies to take when disclosing sustainability information in accordance with SSBJ standards.

The Sustainability Standards Board (SSBJ) is an organization that develops and formulates standards for corporate sustainability information disclosure in Japan. SSBJ standards are guidelines that outline how domestic companies should disclose sustainability information. The SSBJ publishes draft standards equivalent to IFRS S1 and S2, which are international disclosure standards set by the International Sustainability Standards Board (ISSB).

Challenges faced by companies following the mandatory disclosure of SSBJ standards

The SSBJ standards will be applied as early as the securities reports for the fiscal year ending March 2027, making the disclosure of sustainability information mandatory for companies with a market capitalization of 3 trillion yen, and it is expected that this will be gradually extended to companies of varying market capitalization from 2028 onward.

The target companies must comply with the requirements of the SSBJ standards.Third-party assurance of disclosed information (accuracy), simultaneous disclosure with financial information (speed), and disclosure within the same consolidated scope as the financial statements (breadth).To address this, companies will need to take measures equivalent to those they have traditionally taken to disclose financial information in their securities reports. Specifically, in preparation for the mandatory disclosure in the fiscal year ending March 2027, the following three issues must be addressed by 2026.

<Three challenges in collecting and disclosing sustainability information>

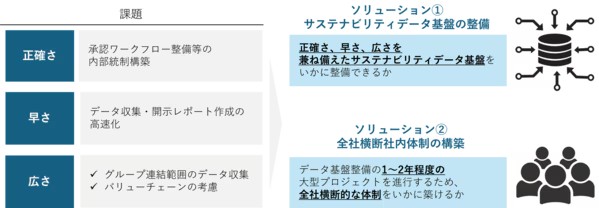

Ensuring the "accuracy" of disclosed information

Sustainability information serves as a criterion for investment decisions in companies, making it necessary to obtain third-party assurance and disclose accurate information. To obtain third-party assurance, it is necessary to disclose information equivalent to financial information.Internal controls, such as establishing an approval workflow for the data to be disclosed, are required.

Ensuring the "speed" of information disclosure

Currently, Japanese companies typically disclose their securities reports in June and their sustainability reports three months later in September. However, after the SSBJ standards are implemented, it will become mandatory to disclose both financial and sustainability information simultaneously in June. Therefore, companies subject to these standards must adapt to a schedule three months earlier than currently in place.We need to expedite the collection of necessary data and the creation of reports that disclose this data.

Responding to the "broadness" of the scope of information disclosure

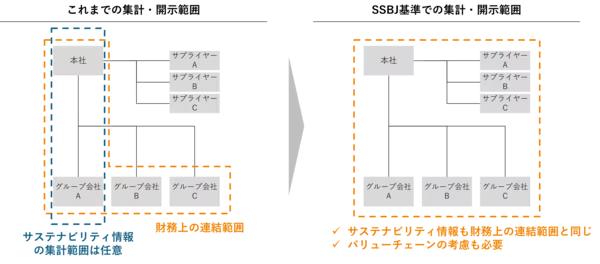

While the scope of disclosure under previous standards could be arbitrarily set by companies, the SSBJ standards require the scope to be group-wide consolidated, similar to financial statements, and also necessitate consideration of the value chain. Therefore,The scope of data collection will be expanded significantly, now including consolidated subsidiaries, including overseas locations, and suppliers.

Effective initiatives for solving problems

This section explains effective initiatives to address the three challenges in collecting and disclosing sustainability information mentioned above.

Solutions for solving problems

[Solution ① Development of a Sustainability Data Platform]

Many companies use Excel for sustainability-related data, but from an accuracy standpoint, it's impossible to set up an approval workflow that can withstand third-party assurance, and from a speed standpoint, it's difficult to expedite simultaneous disclosure with financial information. Furthermore, handling the breadth of data, such as group consolidation and value chains, is expected to require an enormous amount of effort in Excel. Therefore, it is important to establish a sustainability data platform across the entire group.

[Solution ② Establishment of a company-wide internal system]

Developing a data integration platform requires defining the specifications of the data to be collected, making collaboration between the department overseeing sustainability and related departments (Finance and Accounting, Human Resources, General Affairs, Purchasing, Information Systems, etc.) essential. Developing this platform necessitates a large-scale project lasting approximately one to two years, and the key is whether the project can be implemented across the entire company.

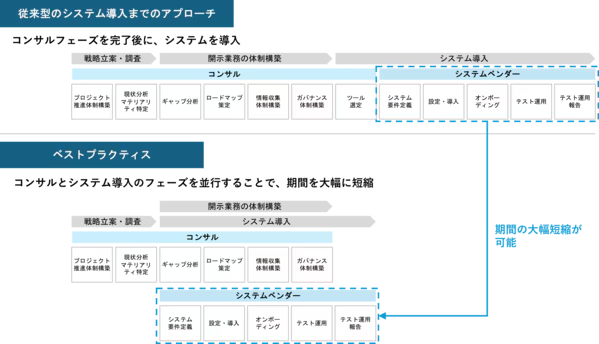

Best practices for establishing solutions

Implementing a system aimed at establishing a data integration platform typically involves completing the consulting phase before starting the system implementation phase, a process that takes at least two years. However, given the requirement to report sustainability information based on SSBJ standards in the securities report for the fiscal year ending March 2027, securing sufficient time is becoming difficult. To shorten the solution implementation period, we recommend, as a best practice, a parallel approach to system implementation starting from the stage where the gap with current operations has been identified during the consulting phase.

summary

To comply with sustainability disclosure regulations, including the SSBJ standards, companies face challenges in terms of accuracy, speed, and scope when collecting and processing data from both internal and external sources. Therefore, measures such as developing a sustainability data collection platform and establishing a company-wide implementation system are necessary. Furthermore, to meet the deadline for the SSBJ standards to come into effect, it is effective to proceed with the consulting and system implementation phases in parallel.

Sustainability 2026 Issue

With the mandatory disclosure requirement coming into full effect in the fiscal year ending March 2027, companies should seize this as an opportunity to implement highly agile management reforms that leverage sustainability data. A crucial turning point for companies will be whether they can establish a data infrastructure, including suppliers, and a system for promoting Sustainability Transformation (SX) by 2026.

Sustainability 2026 Issue: "Making Japan a Leading Nation in SX" Project

Related Pages

Please also read the related pages for this explanation.

For those who want to know about measures to address the SSBJ regulations.

Mandatory Sustainability Information Disclosure: Planned Measures, Targets, and Impacts Explained

This is for those who want to learn about the concept of sustainability management through the use of data.

Data utilization and key points for achieving sustainable management

This is for those who want to know how to calculate greenhouse gas emissions (CO2 emissions, etc.).

How are CO2 emissions calculated?

This is for those who want to know about the process of third-party assurance for greenhouse gas emissions (CO2 emissions, etc.).